Conflicto con Irán: riesgo para los importadores en la cadena de suministro de piezas 4x4

Interrupciones entre Irán y Ormuz: cómo el conflicto afecta la disponibilidad de repuestos para vehículos 4x4, los plazos de entrega y los precios FOB para los importadores en LATAM, África y Medio Oriente.

Conclusion directa

- El contenido para importadores funciona mejor cuando explica insumos de RFQ, restricciones de embarque y pasos de validacion del proveedor.

- El checklist correcto cubre cruce OE, notas de fitment, expectativas de MOQ y metodo de envio antes del pago.

- Las paginas que conectan guia, contacto y producto son mas utiles para compradores y para respuestas de IA.

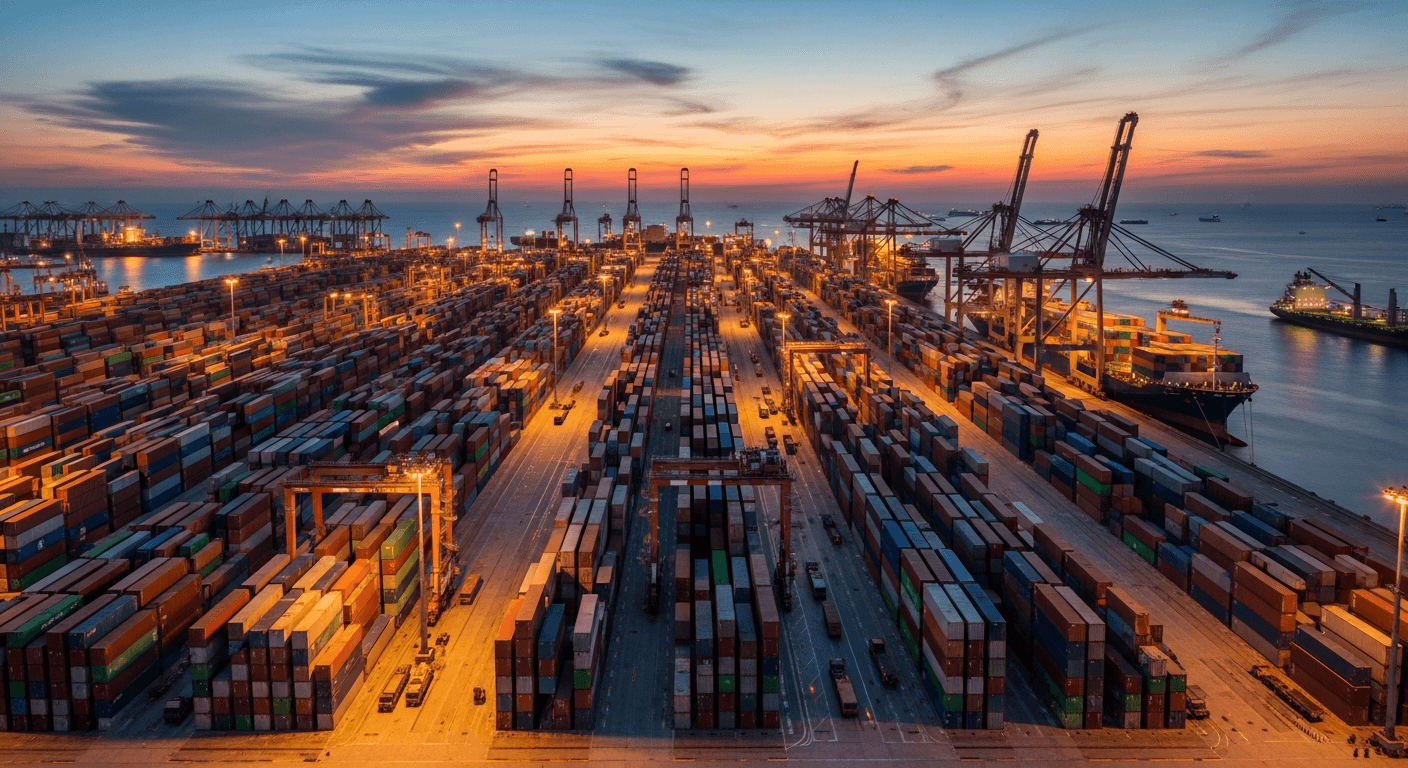

Supply Chain Under Pressure: What the Iran Conflict, Logistics M&A, and Storage Crunch Mean for 4x4 Distributors

Three converging signals — geopolitical disruption, mega-consolidation in freight, and a trailer storage shortage — are restructuring global supply chains. Here is what each one means for your inventory strategy in Q2 2026.

The supply chain pressure triangle

This week's three developments are not isolated events. They form a self-reinforcing pressure triangle. Understanding the structure — not just the headlines — is what separates distributors who act now from those who react in June.

The triangle locks together: higher material costs force longer production lead times; consolidation reduces the frequency and flexibility of shipments; storage demand at ports slows container turnover. Each pressure amplifies the others. Lean inventory models — designed for predictable, efficient markets — are structurally mismatched with this environment.

What happened this week

Three signals arrived simultaneously, each worth tracking on its own. Together, they mark a threshold moment:

Signal 1 — Geopolitical material shock. Roland Berger analysis in Automotive News confirms the Iran conflict is now affecting chemicals, polymers, and specialty materials — not just crude oil. Supply shocks are transmitting from Asia through Europe into the Americas, raising input costs for downstream manufacturers including automotive parts producers in Guangdong (Automotive News RSS).

Signal 2 — Freight market consolidation. Echo Global Logistics completed its acquisition of ITS Logistics, creating a $5.2 billion full-service platform (FreightWaves RSS). When large providers merge, LCL rates — the standard for aftermarket parts importers — typically increase 8–15% as capacity is rerouted toward full-container premium clients.

Signal 3 — Storage demand spike. Retailers and manufacturers are renting temporary trailers at a pace not seen since the 2021 container crisis, driven by tariff uncertainty and nearshoring inventory pre-loading (FreightWaves RSS). This occupies port-adjacent warehouse space and slows container return cycles.

Risk by product category

Not all SKUs carry equal exposure. The risk profile depends on whether the product relies on polymer inputs (high chemical supply sensitivity), steel stampings (relatively insulated), or electronic components (energy and logistics sensitive). Here is our category-level assessment:

| Product Category | Risk Driver | Material Risk | Lead Time Risk | Expected Delay | Recommended Safety Stock |

|---|---|---|---|---|---|

| LED Light Bars & Headlights | Resin housings + electronics | High | High | 12 weeks | |

| Bumpers & Plastic Body Parts | Chemical-dependent polymers | High | High | 14 weeks | |

| Suspension Kits (steel) | Steel stamping — insulated | Low | Medium | 8 weeks (unchanged) | |

| Brake Pads & Rotors | Friction material sourcing | Medium | Low | 10 weeks | |

| Filters & Service Parts | Resin + foam composites | Medium | Medium | 10 weeks |

Steel-based mechanical parts (suspension kits, tow bars, roll bars) are the most resilient category this quarter. Polymer-intensive accessories carry the highest compounded risk because they are simultaneously exposed to chemical input cost increases and longer warehouse dwell times at congested ports.

Regional storage demand surge

Across our distributor network, storage inquiry volume — a leading indicator of anticipated supply disruption — has risen sharply in Q1 2026. Latin America leads, driven by pre-tariff inventory loading and nearshoring-related warehouse displacement at Mexican ports.

The SEA spike (Thailand, Indonesia, Philippines) reflects both tariff positioning and anticipated demand for Hilux and L200 parts ahead of the dry-season fleet overhaul cycle in May. MEA growth is concentrated in UAE-based re-exporters who are pre-loading inventory ahead of potential Hormuz shipping premium increases. Australia remains the most stable market — domestic lead time expectations are longer by default, providing a natural buffer.

Q2 2026 scenario outlook

Three plausible scenarios for Q2, based on how the Iran situation and logistics consolidation evolve. We assign the base case a 55% probability, the bull case 20%, and the bear case 25%.

| Metric | Bull Case (20%) Tension de-escalates Apr |

Base Case (55%) Friction persists Q2 |

Bear Case (25%) Hormuz disruption widens |

|---|---|---|---|

| Shipping rate change (Guangzhou → LatAm) | +5–8% | +12–18% | +25–35% |

| Polymer-based SKU lead time | +1–2 weeks | +3–4 weeks | +6–8 weeks |

| Port dwell time (key hubs) | Normal (4–6 days) | +30–40% (6–9 days) | +70%+ (8–12 days) |

| LCL rate premium post-M&A | +5–8% | +10–15% | +18–22% |

| Recommended safety stock level | 8–10 weeks | 10–14 weeks | 16–20 weeks |

| Action window | Normal reorder cadence | Order before Apr 15 | Order immediately |

Action priority matrix

Not every action carries equal urgency. Plot your decisions on two axes: how quickly you need to act, and how much impact it will have on Q2 supply continuity.

Immediate Distributor Checklist (complete by Apr 10)

- Plastic & LED SKUs first: Place Q2 orders for resin-dependent parts immediately. These face the longest combined lead time risk (+4–5 weeks) and the highest material cost volatility.

- Lock freight rates: Contact your forwarder now to fix Q2 contract rates. Post-consolidation spot rates will likely rise 10–15% by May for LCL shipments.

- Secure warehouse allocation: Confirm Q2 storage slots with your 3PL or bonded warehouse. Trailer rental costs near Manzanillo and Jebel Ali hubs are already rising.

- Add a backup forwarder: Identify one alternative freight partner who is not part of the Echo/ITS network to maintain routing flexibility.

- Deprioritize air freight for heavy parts: Do not spend on air freight for suspension or brake parts — the cost premium (8–12x sea) does not justify it for margin-thin mechanical SKUs.

Editorial judgment

We believe the critical action window is now through April 15. Distributors who complete Q2 restocking by that date will absorb freight and material cost increases at current levels and avoid the stockout risk that will likely emerge between May and June if the base case holds. The supply chain is not broken — it is slowing and becoming more expensive. The cost of carrying extra inventory for 4–6 weeks is a fraction of the cost of losing a customer order to a competitor who stocked ahead. Steel-based mechanical parts are not the priority concern this quarter. Focus your budget and attention on polymer and electronic accessories — that is where margin erosion and availability risk will concentrate.

FAQ

Will shipping rates from Guangzhou increase immediately?

Spot rates are already showing early movement. In our base case, we expect Guangzhou–LatAm rates to rise 12–18% by May. Locking in Q2 contracts before April 15 is the most cost-effective protection. Waiting until late April means accepting whatever the post-consolidation spot market offers.

Which vehicle platforms are most at risk for parts delays?

Platforms with high accessory attachment rates — Hilux and L200 — are most exposed because their accessories (light bars, bumpers, snorkels) are polymer-heavy. Core mechanical parts (suspension, brakes) on these platforms are relatively insulated since they rely on steel stamping rather than chemical-sensitive materials.

Should we switch to air freight for critical stock?

Only for high-margin electronics where a single order justifies the 8–12x cost premium. For suspension kits, brake components, or body armor panels — no. The weight and margin profile makes air freight economically irrational. Instead, order earlier by sea and build the buffer into your lead time planning.

How long will this supply chain pressure last?

In our base case, pressure peaks in May–June 2026 and moderates in Q3 as logistics networks adjust to the new consolidation structure and geopolitical tension stabilizes (or is priced in). Plan for a 3–4 month friction window. Distributors who over-stock now will be in a strong position to take market share during that period.

Sources

Preguntas frecuentes

Que datos deben ir en una primera RFQ a un proveedor de autopartes?

Numero OE, modelo y ano, objetivo de cantidad, mercado destino y si la solicitud es piloto o de reposicion.

Como pueden reducir errores los importadores en pedidos mixtos?

Agrupe la RFQ por linea de vehiculo y sistema, y luego confirme fitment, empaque y metodo de envio antes de liberar.

Fuentes

Productos recomendados para esta guia

Ver catalogo

Rotula superior de suspension

Mitsubishi L200

Brazo inferior delantero derecho

Mitsubishi L200 RH · Mitsubishi L200

Rotula inferior de suspension

Toyota Hilux

Faro delantero izquierdo

Mitsubishi L200 2015+ · Mitsubishi L200